US charges disgraced crypto tycoon Bankman-Fried with ‘massive, years-long fraud’

Prosecutors say founder of cryptocurrency exchange FTX deceived customers and investigators from the company’s start in 2019; could face life in jail

")

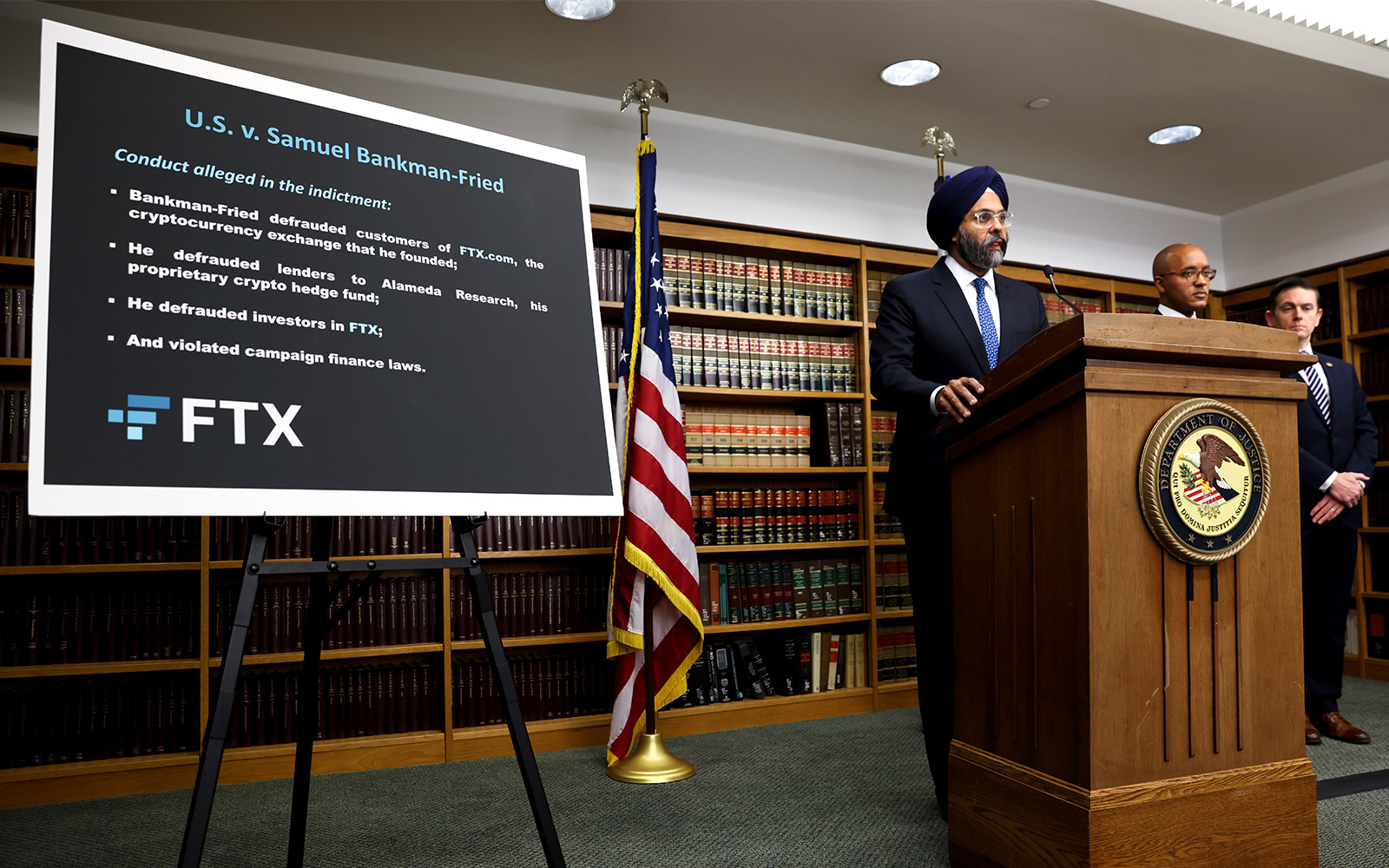

The US government charged Samuel Bankman-Fried, the founder and former CEO of cryptocurrency exchange FTX, with a host of financial crimes on Tuesday, alleging he intentionally deceived customers and investors for years to enrich himself and others, while playing a central role in the company’s multibillion-dollar collapse.

Federal prosecutors said Bankman-Fried devised “a scheme and artifice to defraud” FTX’s customers and investors beginning in 2019, the year it was founded. He illegally diverted their money to cover expenses, debts and risky trades at the crypto hedge fund he started in 2017, Alameda Research, and to make lavish real estate purchases and large political donations, prosecutors said in a 13-page indictment.

Bankman-Fried, 30, was arrested Monday in the Bahamas at the request of the US government and remains in custody after being denied bail.

He has been charged with eight criminal violations, ranging from wire fraud to money laundering to conspiracy to commit fraud. If convicted of all the charges, Bankman-Fried — referred to by crypto enthusiasts as “SBF” — could face decades in jail.

Bankman-Fried “was orchestrating a massive, years-long fraud, diverting billions of dollars of the trading platform’s customer funds for his own personal benefit and to help grow his crypto empire,” prosecutors said.

At a press conference on Tuesday, US Attorney Damian Williams in New York called it “one of the biggest frauds in American history,” and said the investigation is ongoing and fast-moving.

Bankman-Fried has fallen hard and fast from the top of the cryptocurrency industry he helped to evangelize. FTX filed for bankruptcy on November 11, when it ran out of money after the cryptocurrency equivalent of a bank run.

Before the bankruptcy, he was considered by many in Washington and on Wall Street as a wunderkind of digital currencies, someone who could help take them mainstream, in part by working with policymakers to bring more oversight and trust to the industry.

Bankman-Fried had been worth tens of billions of dollars — at least on paper — and was able to attract celebrities like Tom Brady or former politicians like Tony Blair and Bill Clinton to his conferences at luxury resorts in the Bahamas. One prominent Silicon Valley firm, Sequoia Capital, invested hundreds of millions of dollars in FTX.

Sporting shorts and t-shirts to contrast himself with the buttoned-down world of Wall Street, he was the subject of fawning media profiles, a vocal advocate for a type of charitable giving known as “effective altruism,” and garnered over a million Twitter followers.

But since FTX’s implosion, Bankman-Fried and his company have been likened to other disgraced financiers and companies, such as Bernie Madoff and Enron. Authorities say Bankman-Fried lied to customers, investors and lenders about what he was doing with their money since 2019, puncturing his claims that he had only made “mistakes.”

The criminal indictment against Bankman-Fried and “others” at FTX is on top of civil charges announced Tuesday by the Securities and Exchange Commission and the Commodity Futures Trading Commission. The SEC alleges Bankman-Fried defrauded FTX customers by making loans to himself and other FTX executives, and illegally using investors’ money to buy real estate for himself and his family.

No other FTX executives were named in the indictment, nor was the CEO of Alameda Research, Caroline Ellison. Also not named in the indictment: Bankman-Fried’s father, Joseph Bankman, a Stanford University law professor who was considered an adviser to his son.

US authorities said they will try to claw back any of Bankman-Fried’s financial gains from the alleged scheme.

A lawyer for Bankman-Fried, Mark S. Cohen, said Tuesday he is “reviewing the charges with his legal team and considering all of his legal options.”

At a congressional hearing Tuesday that was scheduled before Bankman-Fried’s arrest, the new CEO brought in to steer FTX through its bankruptcy proceedings leveled harsh criticism. He said there was scant oversight of customers’ money and “very few rules” about how their funds could be used.

John Ray III told members of the House Financial Services Committee that the collapse of FTX, resulting in the loss of more than $7 billion, was the culmination of months, or even years, of bad decisions and poor financial controls.

“This is not something that happened overnight or in a context of a week,” he said.

He added: “This is just plain, old-fashioned embezzlement, taking money from others and using it for your own purposes.”

Before his arrest, Bankman-Fried had been holed up in his luxury compound in the Bahamas. US authorities are expected to request his extradition to the US. He will need to be extradited for a federal trial in the US, and the two countries have an extradition treaty, but the process could take months.

Bankman-Fried spent a night in jail and was denied bail at a court hearing in the Bahamas on Tuesday after prosecutors argued he was a flight risk, according to Our News, a broadcast news company based there.

Bankman-Fried was previously one of the world’s wealthiest people on paper; at one point his net worth reached $26.5 billion, according to Forbes. He was a prominent personality in Washington, donating millions of dollars to Democrats and Republicans. US Attorney Williams said Tuesday that Bankman-Fried made “tens of millions of dollars” in illegal campaign donations.

His wealth unraveled quickly last month, when reports called into question the strength of FTX’s balance sheet. As customers sought to withdraw billions of dollars, FTX could not satisfy the requests: their money was gone.

“We allege that Sam Bankman-Fried built a house of cards on a foundation of deception while telling investors that it was one of the safest buildings in crypto,” said SEC Chair Gary Gensler.

The SEC complaint alleges that Bankman-Fried had raised more than $1.8 billion from investors since May 2019 by promoting FTX as a safe, responsible platform for trading crypto assets.

Instead, the complaint says, Bankman-Fried diverted customers’ funds to Alameda Research without telling them.

“He then used Alameda as his personal piggy bank to buy luxury condominiums, support political campaigns, and make private investments, among other uses,” the complaint reads.

In the weeks after FTX’s collapse, but before his arrest, Bankman-Fried gave interviews to several news organizations in which he grasped for ways to explain what happened.

For example, Bankman-Fried said he did not “knowingly” misuse customers’ funds, and that he believes angry customers will eventually get their money back.

At Tuesday’s congressional hearing, the new FTX CEO bluntly disputed those assertions: “We will never get all these assets back,” Ray said.

He said the problems arose because control was “in the hands of a very small group of grossly inexperienced and unsophisticated individuals.”

“Never in my career have I seen such an utter failure of corporate controls at every level of an organization, from the lack of financial statements to a complete failure of any internal controls or governance whatsoever,” said Ray, who also oversaw the collapse of Enron, the energy company that fell apart in a massive scandal in 2001.

Jack Sharman, an attorney at Lightfoot, Franklin & White, said Bankman-Fried’s recent comments to the media could be damaging, admissible evidence in court. “Those statements in that speaking tour were in no way helpful to his cause,” Sharman said.

“If convicted he could be facing the rest of his life in prison, given the dollar amount of the fraud,” Jacob S. Frenkel, a former federal criminal prosecutor at Dickinson Wright, told AFP. “We would not see an indictment if prosecutors were not absolutely convinced that they will win a conviction.”

In its complaint, the SEC challenged Bankman-Fried’s recent statements that FTX and its customers were victims of a sudden market collapse that overwhelmed safeguards that had been in place.

“FTX operated behind a veneer of legitimacy,” said Gurbir Grewal, director of the SEC’s enforcement division. “That veneer wasn’t just thin, it was fraudulent.”

The fall of FTX has caused major doubts about the long-term viability of cryptocurrency and heaped stress on other platforms and entities that rode the success of Bitcoin and other currencies. The company’s collapse — which followed other cryptocurrency debacles earlier this year — is also adding urgency to efforts to regulate the industry.

Yesha Yadav, a law professor at Vanderbilt University who specializes in financial and securities regulation, said US lawmakers and regulators have been too slow to act, but that is likely to change.

“Lawmakers are clearly under pressure to do something, given that so many people have lost their money,” she said.

")

and Sgt. Ohad Yaari, 21.")

")

")

")

")

")

")

The Times of Israel Community.