Israeli blockchain firm develops ‘fire prevention’ tech to thwart FTX-style fraud

StarkWare, valued at $8b, gathers 700 crypto developers in Tel Aviv to explore its tech, which speeds up transactions and is meant to make it impossible for exchanges to loot funds

Sharon Wrobel is a tech reporter for The Times of Israel

with co-founder and CEO Uri Kolodny at blockchain event in Tel Aviv, Feb. 7, 2023. (Courtesy)")

With the collapse of bankrupt crypto exchange FTX still sending shivers through the industry and fueling consumer mistrust, an Israeli multi-billion-dollar startup is making its “uncheatable” blockchain transaction technology available for mass adoption in hopes of preventing the next fraud scandal.

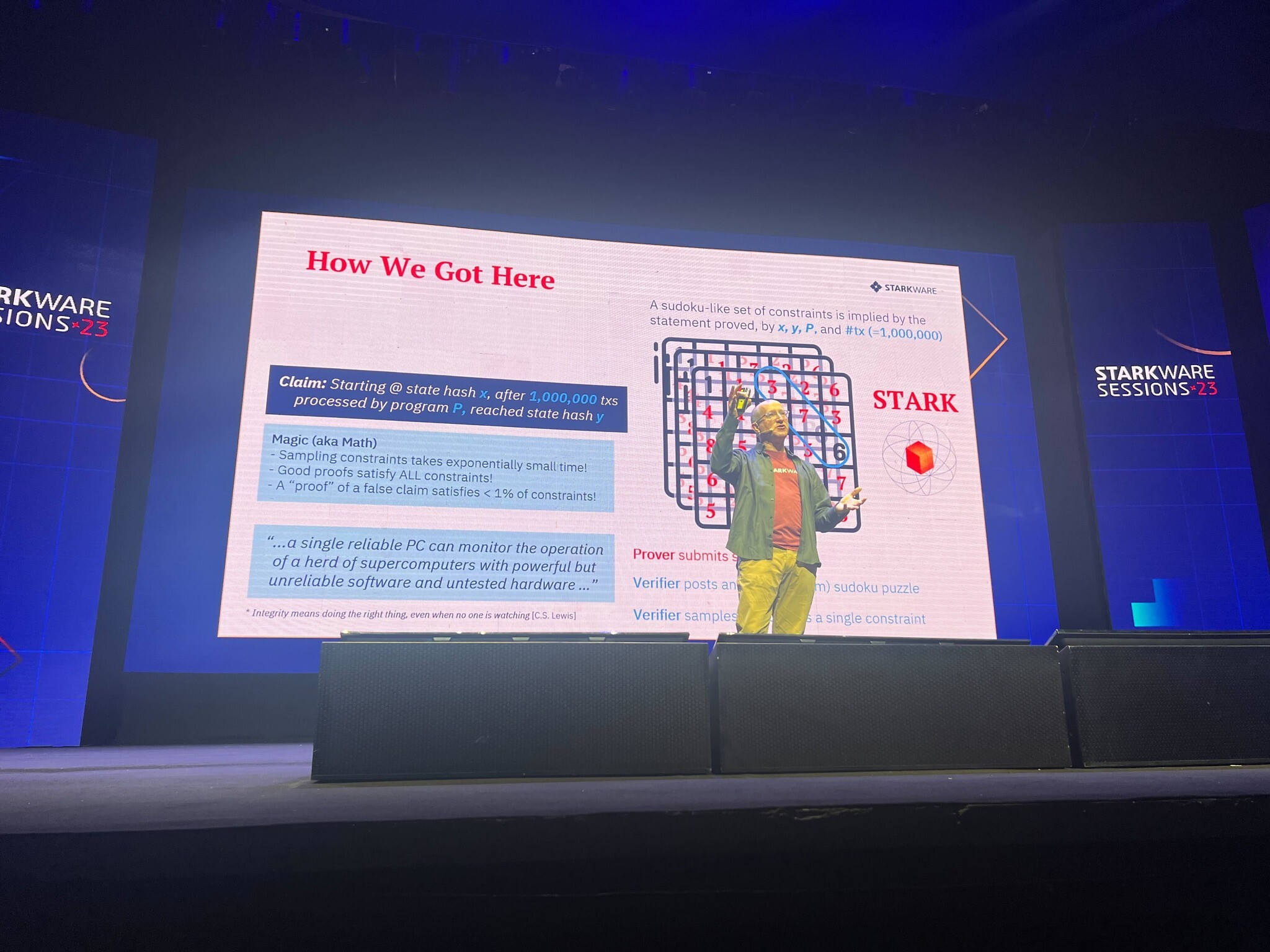

Netanya-based StarkWare, which is valued at $8 billion, is the developer of a technology that compresses and speeds up blockchain transactions. Israeli computer scientist Prof. Eli Ben-Sasson is the mathematical brain behind the Stark technology, which is a proof system based on cryptography and modern algebra powering its two networks, StarkEx and the “blockchain internet” called StarkNet, used for blockchain applications and processing transactions.

The blockchain startup this week gathered a crowd of about 700 crypto developers and coders from around the world in Tel Aviv, where Ben-Sasson, co-founder and president of StarkWare, announced that the core software powering the networks will be open-sourced, meaning that it will be made a public good. It can be used as an infrastructure for all the things that can be deployed today on blockchain, such as payments, exchanges, gaming, NFTs or non-fungible tokens, voting, and governance. Visa Inc., the credit card firm is trying out the tech for making automatic crypto payments.

StarkWare says that its technology, geared to make blockchain scalable for mass adoption, handles more transactions than Bitcoin.

“We’re seeing this Stark technology, which most people haven’t heard of but which will soon underpin the apps we all use, becoming public property,” said Itamar Lesuisse, co-founder and CEO at Argent, a company that built a smart wallet using StarkNet. “This is huge. It’s driving the growth of a big community of people from all over the world who are excited to build on this infrastructure.”

“We’re collectively saying: Let’s shift the paradigm in crypto from ‘please don’t be evil’ to ‘the tech means you just can’t be evil,” said Lesuisse, who was one of the speakers at the blockchain event.

StarkWare said the gathering marked the largest event on new crypto tech since the FTX scandal and focused on exploring blockchain infrastructure that promises to make it impossible for crypto exchanges to misappropriate funds.

Blockchain, the technology that underpins cryptocurrencies, has been suffering from reputational damage since FTX founder Sam Bankman-Fried was charged with illegally diverting massive sums of customer money from his cryptocurrency trading platform for lavish real estate purchases, political donations and risky trades without the knowledge of investors, customers and most employees.

“A lot of people are now talking about things like smoke detectors for the kinds of frauds that went on allegedly at FTX,” Ben-Sasson told The Times of Israel. “Our technology is better than a smoke detector; it is a fire prevention mechanism. It does not allow those who use it to misappropriate funds of their users.”

Blockchain is the database technology underlying bitcoin and other cryptocurrencies allowing for the use of peer-to-peer payment systems. It runs by recording transactions as “blocks” that are updated in real time on a digitized ledger without a central record keeper. Many entrepreneurs and computer scientists see enormous potential of using blockchain for real-world applications as money and other assets can be transferred from person to person without going through a central authority.

Cryptocurrencies are digital currencies that can be exchanged between people without the involvement of intermediaries, like banks or governments. Blockchain is the distributed public ledger that allows these cryptocurrencies to change hands without someone making digital copies of the currency or otherwise tampering with the record of data or ownership.

“We live in a period in which more and more of our financial interactions are mediated by a very small number of very big companies or banks, and there is a growing understanding that it’s not good that all of our money flows are run through Google Pay, or Visa, or banks and that all of our social connections are run through Facebook or Twitter, or Instagram,” said Ben-Sasson. “What blockchain does is really allow us to return to the peer-to-peer nature of social and economic interactions, but do so over the internet.”

“There is no federal reserve of bitcoin, there is no chief banker for Stark or for any of these protocols. These are decentralized protocols and this is the beauty of blockchain,” he added.

StarkWare was co-founded in 2018 by Ben-Sasson, CEO Uri Kolodny, Michael Riabzev and Alessandro Chiesa. In May last year, the startup raised $100 million at a valuation of $8 billion in a series D funding round that was led by Greenoaks Capital and Coatue, and included Tiger Global. That’s up from the $2 billion valuation at its last fundraise in November 2021.

According to Ben-Sasson, what happened at FTX and with other similar catastrophic failures is that people handed over control of funds to the exchange and were promised that they wouldn’t be misappropriated.

“Now, our technology uses the blockchain to enforce self-custodial trading, meaning that the customers working over our technology always are in control of their funds so it is impossible to misappropriate funds over our technology,” he explained.

StarkEx and Starknet are so-called “Layer 2” networks that run over the Ethereum blockchain, which anchors their security. They have processed more than $800 billion in transactions, and provide the infrastructure for Immutable X, a developer platform for web3 games; Sorare, a fantasy sports gaming experience based on NFTs; and dYdX, a decentralized exchange for the trading of crypto derivatives.

“The StarkNet ecosystem has the potential to get the next billion people using crypto and enable people to get started with no technical knowledge because we are making that leap to an affordable and friendly user experience,” said Motty Lavie, founder and CEO of smart contract wallet provider Braavos. “We can bring this intuitive and simple experience to what we call self-custodial wallets, meaning crypto which is fully in your control and nobody can get their hands on your funds.”

“It gives more people the confidence to use self-custodial solutions and not to default to centralized players, like FTX and others,” Lavie said.

Ben-Sasson is not too concerned about the bad reputation the cryptocurrency and blockchain space often suffers from, saying it is only natural that because of its potential and hype that it has attracted its fair share of bad actors.

“I’m not worried about the image. I think more and more people understand and know that the core technology is really robust and is here to stay,” Ben-Sasson noted. “It’s not blockchain that caused the collapse but it is the companies that were either fraudulent or just very negligent and misappropriated user funds.”

Ben-Sasson said the crypto crisis draws parallels with the dot-com shakeout of the early 2000s, out of which companies like Twitter Inc. and Facebook eventually rose.

“Going forward, I believe blockchain will be a strata used for social and financial interactions and agreements,” said Ben-Sasson. “The number of followers on Twitter or Instagram, meaning your social persona, will be your own one day on blockchain, and your financial transactions and your credit history are not going to be owned and maintained by some external party’s data. They will be yours, proven by you on a blockchain.”

")

")

")

")

")

")

")

")

The Times of Israel Community.