Better mortgage conditions may help more homebuyers get a leg up, experts say

Easing Israel’s strict caps on lending, meant to insulate the financial sector, could unlock home ownership for first-timers who don’t have the ‘bank of mom and dad’ to rely on

")

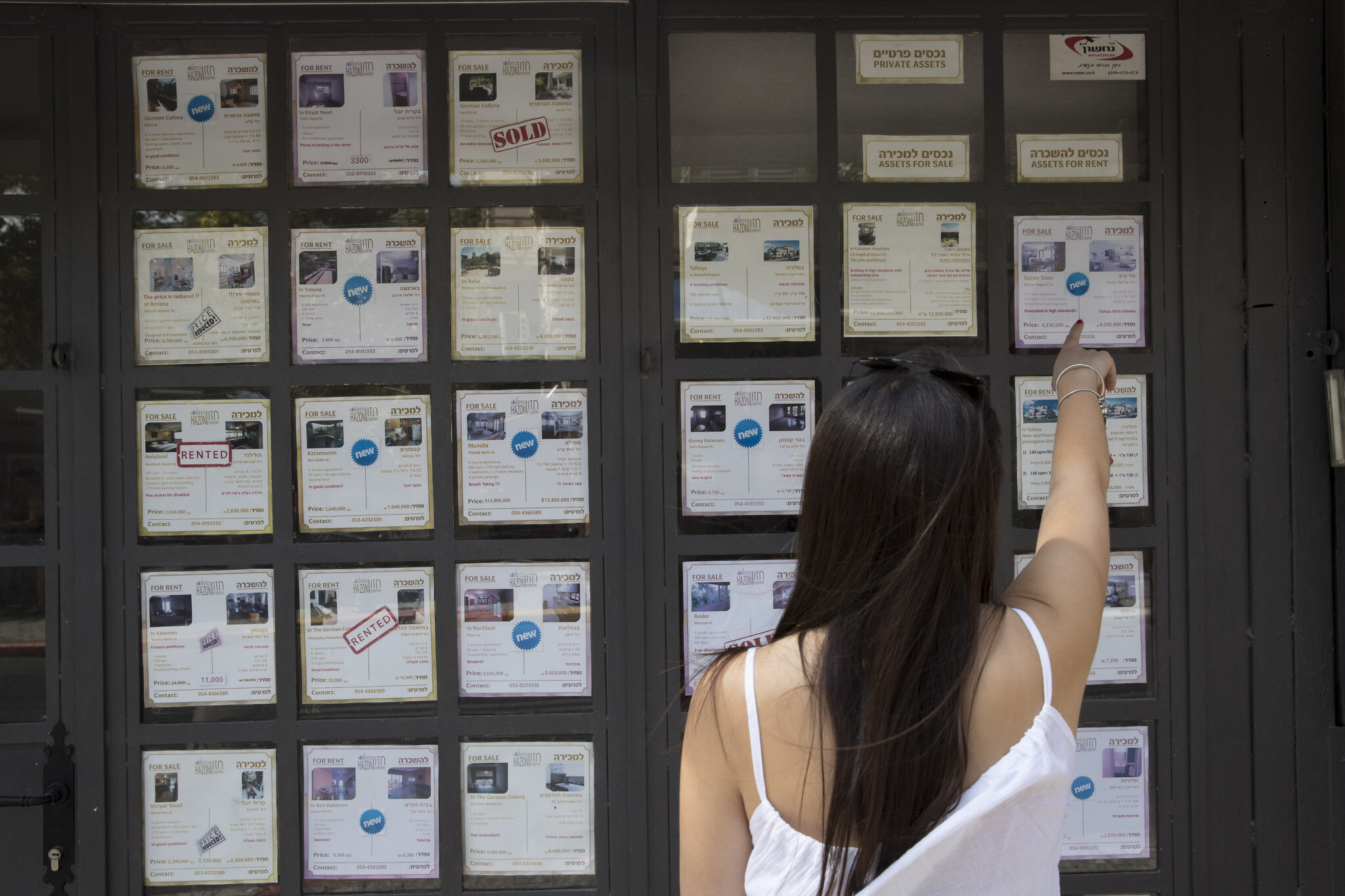

Policymakers seeking to slow the inexorable rise in housing prices recently began turning their attention to an often-overlooked piece of Israel’s homebuying puzzle: mortgages.

Unlike many other countries, where banks can cover 90 percent or even all of a home loan, in Israel lenders are prohibited by Bank of Israel regulations from covering more than 75 percent of a housing loan. But some have begun to question the wisdom of the cap as well as other regulations aimed at protecting banks from risky loans, which have ended up locking many would-be buyers out of their first home.

That loan cap means the average homebuyer needs a nest egg of NIS 510,000 ($152,000) plus enough extra to cover agent fees, legal fees, and the property purchase tax to secure an average home for NIS 1,757,000 ($505,840) based on the price of an average property in Israel, as of March 2022. In Tel Aviv, where the average home goes for NIS 2,505,000 ($721,189), homebuyers need over NIS 700,000 ($200,000) stashed under the mattress.

“The Bank of Israel borrowing limits mean that a large number of those in their 30s and 40s, even if they are earning well above the national average and able to afford the repayments on a mortgage of NIS 3 to 4 million ($943,000 to $1.3 million), cannot buy a property in the center of the country,” said Norman Shapiro, a senior mortgage broker with First Israel Mortgages.

“What is happening is that a substantial proportion of the population is being socially engineered out of the housing market,” he told The Times of Israel.

Before the Knesset disbanded last month, MK Michael Biton, head of the Knesset Economics Committee, called for regulators and banks to be allowed to increase the percentage of a property’s price they can loan out, as a way to allow homebuyers to keep pace as housing costs soar.

After a Bank of Israel representative told a June 19 Economics Committee meeting that only some 0.02% of home loans run into serious issues, Biton indicated that the relatively minor risk may not warrant the strict regulation.

“We don’t want too much risk and a bubble to burst, as occurred in the US in 2008, but looking at these figures — which show that we have over 99% stability — why not raise the credit cap to 80%?” he asked.

Regulators have instead gone the other way, raising interest rates to hamstring lending and slow down inflation. After years of rates being kept as low as possible, the bank has raised rates three times over the past several months, to 1.25%. Banks have in turn raised rates for borrowers, and the costs of taking out a loan to buy a home have rapidly increased.

A 30-year fixed rate mortgage carries interest of between 4.75% and 5.10% (compared to 3.8% six months ago) and a variable rate is around 2.75% (up from 1.6% six months ago), according to market research by Shapiro and fellow leading mortgage specialist Aaron Krasner of Anglo Mortgages.

The rates don’t only make home ownership more expensive, but also affect who banks are allowed to lend to, thanks to the Bank of Israel’s limit on how much of a monthly salary can be used to pay a mortgage.

The cap varies between 33% and 40% of net monthly income after tax, and after any other debt commitments a borrower may have.

To qualify for a monthly mortgage of NIS 10,000 ($2,870), a borrower would need to net at least NIS 25,000 ($7,175) a month. With the average monthly wage after taxes in Israel around NIS 7,700 ($2,200), it’s a threshold even many two-earner households will struggle to reach.

While designed to shield banks from bad loans and keep borrowers from overstretching themselves, the regulation has wound up forcing some homebuyers to take longer mortgages, or sign up for riskier, but cheaper, variable interest rates for part of the mortgage.

Strict caps on loan-to-value can be found in 40% of developed countries, according to researchers at Tel Aviv University. They help to slow down growth in household debt and reduce bank losses if housing markets crash. They have no impact on house prices, but they undoubtedly make it harder to get onto the housing ladder.

“The Bank of Israel is nervous that the housing market crashes seen in other parts of the world could happen here, and in those cases the banking sector as a whole has taken a big hit. It wants to protect banks from that kind of exposure, but by doing that, it is making life more difficult for buyers,” Shapiro said.

In markets such as the US and the UK, first-time buyers can borrow 90% or even 100% of the cost of a new home. Some loans are structured to also include additional property purchase costs, which Israeli regulations also prohibit.

These deals are not available for everyone: applicants generally need a good credit history and mortgage insurance, and will pay a higher rate of interest. But these kinds of loans can allow younger people with good salaries to buy their first property with a relatively small initial cash investment.

In Israel, the average age of a first-time purchaser is 36, relatively high for the West.

“A decade ago, Israeli insurance companies offered additional financing for home purchases,” Shapiro said. But, he goes on to explain, “the Bank of Israel became concerned about the risks of people borrowing more against property, and in 2012 they stepped in to impose clear limits on borrowing, capping loans to first-time buyers at 75% and explicitly stating that banks may not provide additional loans to cover equity for purchasing property.”

The Bank of Israel maintains that housing debt in Israel is relatively low by international standards and that the conditions it has set for mortgages are conservative compared to other similar economies, but it wants to ensure Israel’s financial system is risk-resilient to the housing market, explained Shapiro.

With a 75% loan cap, banks’ exposure to negative equity is minimized, taking on board the lessons of the 2007-2008 mortgage bubble crash.

Borrowing limits also encourage purchases in cheaper parts of the country, and limits on mortgages on second properties help to dampen the enthusiasm to buy additional investment properties.

So far the Bank of Israel has set out to help would-be homeowners mainly by encouraging transparency in the mortgage market to allow buyers to understand overall costs and get the right deal for them.

Last year, Israelis borrowed a record NIS 116 billion ($36.5 billion) in mortgage loans. In part, this was because of record price increases in the cost of property — up more than 15% so far this year, according to the Central Bureau for Statistics. The limits on how much they can borrow to fund a mortgage, however, mean that overall household debt is relatively low in Israel compared to other countries, but that it is also harder to buy a home.

Home sales peaked in late 2021 after rising steadily since 2018, but the market has shown signs of retreating since then. New home sales during the period from February to April 2022 were 12.9% lower than the three months previous, according to seasonally adjusted government figures. Demand for new homes was down 8.6%.

According to Krasner, the market relies heavily on the ability of buyers to marshal intergenerational wealth.

“This system only works because in Israel most people buying first homes are getting funding for the down payment from their parents,” he said. “They can’t possibly put the money together on their own, so what happens is that the older people who bought property years ago, and have therefore made significant money on it, use some of that value to help their children. It’s obviously not a fair system as some people don’t have parents able to give them that kind of money, but that is what happens.”

The outgoing government attempted to deal with the problem by instituting a lottery program known as “target price,” offering thousands of apartments at rates up to 20% below market value, essentially lopping off part of the down payment and allowing buyers to increase the loan-to-value ratio. It has also focused on increasing supply to bring down prices. Plans are in place for 280,000 new homes in the next three years, with planners expected to approve 500,000 more homes as well during that period. Housing starts are already up massively.

But with so much pent-up demand for homes, and barriers to stepping onto the property ladder, these moves are unlikely to materially change the shape of the housing market.

“Having a home is likely to continue to be restricted to those on extremely high salaries, or with access to the ‘bank of mom and dad’ — neither of which seems to deliver the housing reforms we have been promised,” said Krasner.

However, changing the limits around home borrowing could be a safe way to increase the numbers who can afford a home today, according to experts.

“There are many small changes to the system that a government or the Bank of Israel could make that would help to open up home buying to more people,” Shapiro said.

Among the proposed changes would be one that allows those who earn enough to borrow more than 75% of the property value, for an added tariff. This would reduce the amount they need to offer as a down payment, making it easier for young people in good jobs to buy a home without adding substantial risk to lenders.

Another option would be to allow those taking mortgages to choose — or at least to be evaluated by bankers — as to how much of their monthly income they can reasonably pay as a mortgage. At the moment this is decided for them by the banks, based on monthly household salaries. But high earners, those with more irregular income, those with significant investments, or those with good future prospects could perhaps pay more, or be allowed to take out more flexible loans that see payments increase as they get older.

Although primarily of benefit to higher earners, another possibility would be to allow individuals to take some kind of separate, shorter and probably more expensive personal loan to help fund the down payment and closing costs.

Building more homes, as the government has promised, can make a difference over time. But building enough new homes for everyone at prices everyone can afford is nearly impossible, according to industry experts. Making changes in the loan market could be a faster and more certain way to increase access to homeownership for those still waiting to get a foot in the door.

“All the debate focuses on prices,” said Krasner. “But we need to accept that almost certainly these will continue to go up and to focus instead on helping people to find a way onto the property ladder.”

")

")

")

; Right: US President Donald Trump in the Oval Office of the White House in Washington, June 4, 2026. (AP Photo/Julia Demaree Nikhinson)")

")

")

")

")

The Times of Israel Community.